Are you struggling under the weight of debt? Feeling overwhelmed by credit card bills, student loans, or medical debt? The prospect of debt forgiveness might seem like a lifeline, offering a fresh start and the potential to reclaim your financial future. However, before you jump to conclusions, it’s crucial to understand the complexities and potential implications of pursuing debt relief. This article explores the various avenues for debt forgiveness programs, the pros and cons of each, and ultimately helps you determine if debt forgiveness is the right choice for your unique financial situation.

Navigating the world of debt management and debt solutions can be daunting. This guide will provide you with a clear understanding of different debt relief options, including bankruptcy, debt settlement, and government programs that offer debt forgiveness. We’ll examine the qualifications, requirements, and long-term consequences associated with each option, empowering you to make an informed decision. Learn how to assess your financial health, evaluate your debt-to-income ratio, and ultimately choose the path that best aligns with your financial goals and long-term financial stability.

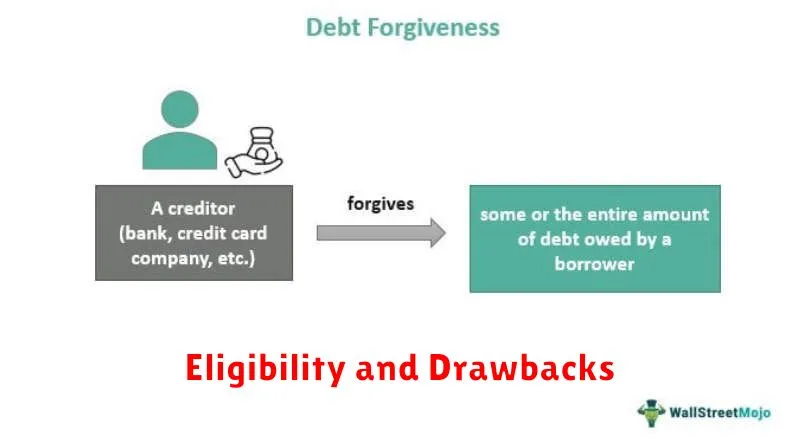

What Is Debt Forgiveness?

Debt forgiveness, also known as debt cancellation or debt relief, is the act of eliminating a debt obligation. This means a creditor, such as a bank or credit card company, agrees to write off a portion or all of the outstanding balance owed by a debtor.

It’s important to differentiate debt forgiveness from other forms of debt relief, such as debt consolidation or debt management plans. These strategies aim to manage debt more effectively, while forgiveness permanently removes the debt.

There are several ways debt forgiveness can occur. It might be offered by a creditor as a settlement option, especially when a debtor is facing financial hardship and unable to make payments. It can also be the result of a bankruptcy proceeding, where a court order discharges certain debts. In some cases, governments may implement programs that offer debt forgiveness for specific types of debt, such as student loans or mortgages, to stimulate the economy or provide relief during a crisis.

While debt forgiveness can provide significant financial relief, it’s crucial to understand the potential implications. For example, debt forgiveness may have tax consequences; the forgiven amount might be considered taxable income. Furthermore, it can negatively impact your credit score, though the effect can vary depending on the circumstances and the type of debt forgiven.

The process of obtaining debt forgiveness can be complex and often requires negotiation with creditors. Understanding your rights and options is essential before pursuing this route.

Types: Student Loans, Credit Cards, Medical

Debt forgiveness programs typically target specific types of debt, each with its own characteristics and implications. Understanding these differences is crucial before considering participation in any such program.

Student loans represent a significant portion of outstanding debt for many individuals. These loans often accrue interest over time, leading to a substantial increase in the overall amount owed. Forgiveness programs targeting student loans may be need-based, income-based, or tied to specific professions (like teaching or public service).

Credit card debt is another prevalent type of debt often targeted by forgiveness initiatives, although less commonly than student loans. High interest rates and aggressive collection practices often make credit card debt particularly burdensome. Credit card debt forgiveness may be offered through settlement programs or as part of broader bankruptcy proceedings.

Medical debt is frequently a source of significant financial strain, particularly for those without adequate health insurance. Unexpected medical expenses can quickly lead to overwhelming debt. Forgiveness programs for medical debt are often less common and may be linked to specific charities or non-profit organizations.

Eligibility and Drawbacks

Eligibility for debt forgiveness programs varies widely depending on the specific program and the type of debt. Income-driven repayment plans, for example, often have income and family size requirements. Federal student loan forgiveness programs may have stipulations about the type of loan, the length of repayment, and the borrower’s employment history (e.g., working in public service). It’s crucial to thoroughly research the specific program’s eligibility criteria before applying.

While debt forgiveness can offer significant relief, it’s essential to acknowledge potential drawbacks. One significant concern is the tax implications. Forgiven debt is often considered taxable income, potentially resulting in a substantial tax bill. This can negate some or all of the financial benefits of forgiveness. Additionally, some programs might have negative impacts on credit scores, especially if the forgiven debt was previously reported as delinquent.

Another potential drawback is the long-term financial implications. While freeing up immediate cash flow, forgiveness doesn’t address the underlying causes of debt accumulation. Without changes to spending habits and financial management, borrowers may find themselves in debt again. Furthermore, the availability of future debt forgiveness programs is uncertain, and relying on them may not be a sustainable long-term strategy.

Administrative complexities can also be a significant barrier. The application processes for debt forgiveness programs can be lengthy and involve considerable paperwork. The requirements for documentation and verification can be demanding, potentially leading to delays and frustration. Navigating the complexities of the process may require professional assistance, adding to the overall cost.

Tax Implications to Understand

One crucial aspect to consider before accepting debt forgiveness is the potential tax implications. The Internal Revenue Service (IRS) generally treats forgiven debt as taxable income, meaning you may owe taxes on the amount of debt that’s forgiven.

This can be a significant financial burden, especially if the forgiven amount is substantial. The tax liability is typically calculated based on your marginal tax rate, which means the tax owed will depend on your overall income level.

However, there are some exceptions to this rule. Certain types of debt, such as debt discharged in bankruptcy, may be excluded from taxable income under specific circumstances. Similarly, debt forgiven due to insolvency—where your liabilities exceed your assets—may also be exempt from taxation.

It’s important to carefully review your specific situation and consult with a tax professional. They can help you determine if the forgiven debt will be taxable and, if so, how to plan accordingly. Understanding these tax consequences is crucial to making an informed decision about accepting debt forgiveness.

Failing to account for these tax liabilities can lead to unexpected tax bills and penalties. Proper planning, including setting aside funds to cover potential tax obligations, is essential to avoid financial distress.

Furthermore, the documentation related to the debt forgiveness is crucial in claiming any applicable exclusions or deductions. Maintaining accurate records of all communications and agreements with creditors is vital for supporting any tax filings.

Alternatives to Try First

Before exploring debt forgiveness, it’s crucial to consider alternative solutions that may be less drastic and potentially more beneficial in the long run. These options can help you manage your debt without resorting to forgiveness, which often carries significant drawbacks.

One primary alternative is debt consolidation. This involves combining multiple debts into a single loan with potentially lower interest rates, simplifying repayment and reducing overall interest paid. Carefully compare offers and interest rates before deciding.

Another valuable strategy is budgeting and financial planning. Creating a detailed budget allows you to identify areas where you can reduce spending and allocate more funds towards debt repayment. Professional financial advice can be invaluable in developing a personalized plan.

Negotiating with creditors can also yield positive results. You might be able to negotiate lower interest rates, reduced monthly payments, or a different repayment plan that better suits your circumstances. Be prepared to demonstrate your commitment to repayment.

For those facing extreme financial hardship, exploring options like debt management plans (DMPs) offered by credit counseling agencies might be helpful. These plans consolidate debts and negotiate with creditors on your behalf, offering a structured approach to repayment.

Finally, understanding and utilizing available government assistance programs should be considered. Depending on your circumstances, you may be eligible for programs that can help alleviate your debt burden. Researching available options in your area is highly recommended.

Where to Find Legit Programs

Navigating the world of debt forgiveness programs can be challenging, as many illegitimate operations prey on vulnerable individuals. Therefore, it’s crucial to exercise caution and only engage with reputable sources.

One of the most reliable avenues is through the government. Federal programs like the Public Service Loan Forgiveness (PSLF) program and Income-Driven Repayment (IDR) plans offer legitimate paths to debt relief. Information about these programs is readily available on official government websites. Thoroughly investigate the eligibility requirements and application processes before participating.

Another trustworthy resource is non-profit credit counseling agencies. These organizations provide free or low-cost guidance on managing debt and may offer assistance with navigating government programs or exploring debt management strategies. Be sure to verify their legitimacy with organizations like the National Foundation for Credit Counseling (NFCC) before seeking their assistance.

It’s essential to be wary of companies promising quick fixes or guaranteed debt forgiveness. Legitimate programs rarely offer such assurances. Avoid any program that requests upfront fees or guarantees unrealistic outcomes. Always verify the credentials and reputation of any organization before sharing personal financial information.

Remember, thoroughly researching and understanding the terms and conditions of any debt forgiveness program is paramount. Seeking guidance from trusted financial professionals, such as certified financial planners, can also provide valuable insights and support.

{kind=link}