Understanding your credit score is crucial for securing loans, mortgages, and even credit cards with favorable terms. A strong credit score can save you thousands of dollars over your lifetime by unlocking lower interest rates and better financial opportunities. This article will delve into the intricacies of credit score calculation, explaining the key factors that influence your creditworthiness and how you can improve your credit report.

Many people are curious about how their credit scores are determined and what they can do to improve them. This comprehensive guide will break down the credit scoring models used by major credit bureaus, such as FICO and VantageScore. We’ll examine the five key components that make up your credit score: payment history, amounts owed, length of credit history, new credit, and credit mix. Learning how these factors impact your score empowers you to take control of your financial future and achieve a higher credit rating.

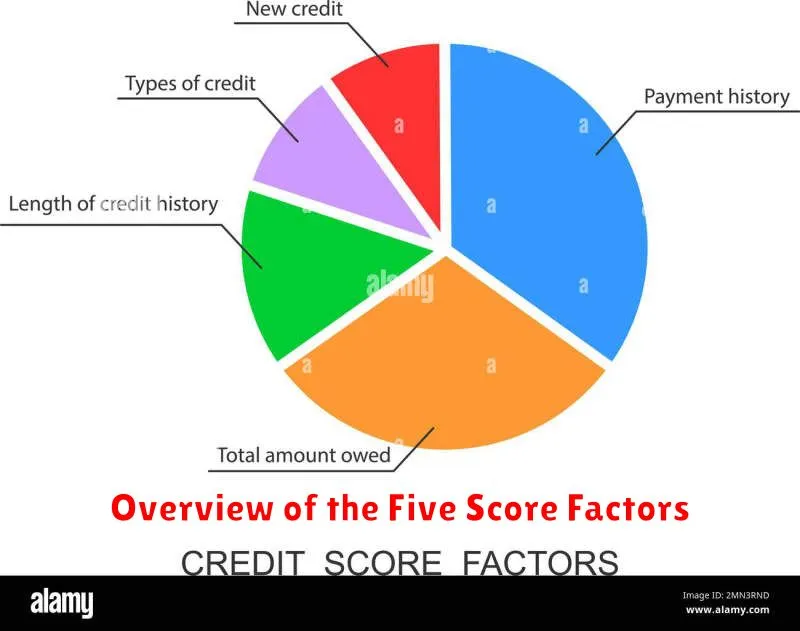

Overview of the Five Score Factors

Understanding how your credit score is calculated is crucial for managing your finances effectively. The most widely used scoring models, such as FICO® Scores, rely on five key factors, each weighted differently to determine your overall score. These factors are not equally important; some have a significantly larger impact than others.

Payment History is the most influential factor, typically accounting for 35% of your credit score. This reflects your record of paying bills on time. Even one missed payment can negatively impact your score, while a consistent history of on-time payments significantly boosts it. Late payments, collections, and bankruptcies all fall under this category.

Amounts Owed, representing 30% of your score, examines how much debt you currently have relative to your available credit. This is often expressed as your credit utilization ratio. Keeping your credit utilization low (ideally under 30%) is beneficial, as high utilization suggests a higher risk to lenders.

Length of Credit History contributes 15% to your score. This factor considers the age of your oldest account and the average age of all your accounts. A longer credit history, demonstrating responsible credit management over time, generally results in a higher score. Opening and closing accounts frequently can negatively impact this aspect.

New Credit accounts for 10% of your score and considers how many new credit accounts you’ve opened recently. Applying for multiple new credit accounts in a short period can temporarily lower your score, as it suggests increased risk to lenders. This is because each application results in a hard inquiry on your credit report.

Finally, Credit Mix makes up the remaining 10% of your score. This refers to the variety of credit accounts you possess, such as credit cards, installment loans (e.g., auto loans, mortgages), and other forms of credit. A diverse credit mix can demonstrate responsible credit management, though it is the least significant factor.

Payment History and Its Weight

Your payment history is the most crucial factor in determining your credit score. This section of your credit report reflects your record of paying bills on time, representing approximately 35% of your total credit score.

Credit bureaus meticulously track your payment behavior across various credit accounts, including credit cards, installment loans (like auto or personal loans), and mortgages. Even seemingly minor late payments can significantly impact your score. A single missed payment can remain on your report for seven years, negatively affecting your creditworthiness during that period.

The severity of the negative impact depends on the number of missed payments and their timing. Multiple late payments or patterns of consistently late payments will result in a more substantial credit score reduction than an isolated incident. Conversely, a consistent record of on-time payments significantly boosts your credit score and demonstrates financial responsibility to lenders.

It’s important to note that even if a payment is made late but within the grace period (the period allowed for late payment before it’s reported to credit bureaus), it may still have a minor negative impact. Therefore, paying bills on time and in full is paramount to maintaining a high credit score.

The information used to assess your payment history comes directly from your creditors. Accuracy is essential; regularly reviewing your credit reports helps identify any discrepancies and allows you to correct any inaccurate information that could negatively impact your score.

Utilization Ratio Explained Clearly

Your credit utilization ratio is a crucial factor in determining your credit score. It represents the percentage of your available credit that you’re currently using. For example, if you have a credit card with a $1,000 limit and you owe $500, your utilization ratio is 50%.

Credit scoring models generally view a lower utilization ratio more favorably. A high utilization ratio suggests you may be overextended financially, increasing the risk of default. Conversely, a low ratio demonstrates responsible credit management.

The ideal utilization ratio is typically considered to be below 30%, with some experts recommending aiming for under 10%. However, the specific impact of utilization ratio varies slightly depending on the credit scoring model used.

Calculating your utilization ratio is straightforward: divide your total credit card debt by your total available credit. For instance, if you have $2,000 in credit card debt and a total available credit of $10,000, your utilization ratio is 20% ($2,000 / $10,000 = 0.20 or 20%).

It’s important to monitor your utilization ratio across all your credit accounts, as this is the figure used in your credit score calculation. Paying down your balances can significantly improve your ratio and, consequently, your credit score.

Remember that your utilization ratio is updated regularly as your balances and available credit change. Consistent, responsible credit card usage contributes to a healthier utilization ratio and a stronger credit score.

Credit Age and New Inquiries

Your credit age, or the length of your credit history, is a significant factor in your credit score calculation. Lenders view a longer credit history as a positive indicator of responsible credit management. A longer history demonstrates your ability to consistently manage credit over an extended period. The age of your oldest account, as well as the average age of all your accounts, are considered.

Conversely, numerous new inquiries within a short time frame can negatively impact your score. Each time you apply for credit, a hard inquiry is placed on your credit report. Multiple inquiries suggest you may be seeking more credit than you can manage, raising a red flag for lenders. While a single inquiry usually has minimal impact, a cluster of inquiries within a few weeks can significantly lower your score.

It’s important to note that the impact of new inquiries and credit age varies depending on the specific credit scoring model used. However, both factors consistently play a crucial role in determining your overall creditworthiness.

To maintain a healthy credit score, it’s advisable to limit applications for new credit and carefully manage existing accounts. Establishing and maintaining a long credit history is key to building a strong credit profile.

Types of Credit You Use

Your credit score is significantly influenced by the types of credit you utilize. Lenders assess the diversity of your credit accounts to gauge your creditworthiness. A well-rounded credit profile typically includes a mix of different credit accounts, demonstrating responsible management across various financial products.

Revolving credit, such as credit cards, offers a line of credit that can be used repeatedly up to a certain limit. Responsible management of revolving credit, characterized by consistently paying your balance on time and keeping your credit utilization low, is a key factor in building a strong credit score.

Installment credit, on the other hand, involves borrowing a fixed amount of money that is repaid over a set period with regular, scheduled payments. Examples include auto loans, mortgages, and personal loans. Consistent on-time payments on installment loans demonstrate your ability to manage debt responsibly over an extended period.

The presence of both revolving and installment credit in your credit report signals to lenders a broader experience with different types of credit accounts, suggesting a more responsible and well-managed credit history. This variety contributes positively to your overall credit score. The absence of either type, or an overreliance on a single type, could negatively impact your score.

Beyond these two main categories, other credit types may be considered, such as open-ended credit lines or secured loans. While less common, these account types can still influence your score. It’s crucial to maintain responsible usage across all credit accounts you hold to optimize your credit health.

How to Track and Improve Score

Understanding your credit score is crucial for financial well-being. Regularly monitoring it allows you to identify potential problems and take proactive steps to improve your standing.

Many services offer free credit score access. These typically provide a simplified version of your score, along with some basic insights into the factors affecting it. However, for a more comprehensive understanding, consider using a paid service that offers detailed reports and explanations.

Once you have access to your score, review the contributing factors. Payment history is the most significant element, accounting for a substantial portion of your overall score. Consistent, on-time payments are paramount. Even a single missed payment can negatively impact your score.

Amounts owed, or your credit utilization ratio, is another key factor. Keeping your credit card balances low, ideally below 30% of your total available credit, is essential. High utilization signifies greater risk to lenders.

The length of your credit history is also considered. A longer history demonstrates a proven track record of responsible credit management. Avoid closing old accounts unless absolutely necessary, as this can shorten your credit history and potentially lower your score.

New credit applications can temporarily lower your score. Numerous applications within a short period suggest increased risk to lenders. Avoid applying for multiple credit lines simultaneously unless truly needed.

Finally, the credit mix, which refers to the variety of credit accounts you hold (e.g., credit cards, installment loans, mortgages), is also considered, though to a lesser extent. A diverse mix may demonstrate responsible credit management across different account types.

By understanding these factors and consistently monitoring your credit report, you can identify areas for improvement and take steps to build and maintain a strong credit score. This will improve your financial opportunities and access to credit in the future.

{kind=link}