Effectively tracking your financial progress monthly is crucial for achieving your financial goals. Whether you aim for debt reduction, saving for a down payment, or simply improving your financial health, consistent monitoring provides valuable insights into your spending habits, investment performance, and overall financial well-being. This guide will provide you with a practical, step-by-step approach to monitor your finances on a monthly basis, empowering you to make informed decisions and stay on track toward your objectives.

Understanding your monthly cash flow is the cornerstone of effective financial tracking. By meticulously monitoring your income and expenses, you gain a clear picture of where your money is going. This process allows for the identification of areas where you can potentially reduce spending, increase savings, and ultimately accelerate your progress towards your financial aspirations. Implementing a robust budgeting system and utilizing financial tracking tools will significantly simplify this process and provide the data you need to make informed choices regarding your financial future.

Define Your Key Money Metrics

Tracking your financial progress requires more than just looking at your bank balance. To effectively monitor your financial health, you need to define key money metrics that are relevant to your financial goals. These metrics will serve as your guideposts, showing you whether you’re on track or need to make adjustments.

Consider what’s most important to you. Are you focused on paying off debt? Then metrics like debt-to-income ratio and minimum payments vs. extra payments are crucial. If saving for a down payment on a house is your priority, track your savings rate and the growth of your savings account. For those aiming for early retirement, net worth and investment returns become key indicators.

Beyond the big picture, consider more granular metrics. Tracking your monthly spending in different categories (housing, food, transportation, etc.) helps identify areas where you can potentially cut back. Monitoring your income sources, whether it’s salary, freelance work, or investments, will give you a comprehensive view of your cash flow. The specific metrics you choose should be tailored to your individual circumstances and objectives.

Remember to choose a manageable number of metrics. Overwhelming yourself with too much data can be counterproductive. Start with 3-5 key metrics and gradually add more as you become more comfortable with the process. The goal is to gain a clear understanding of your financial situation, not to get bogged down in endless spreadsheets.

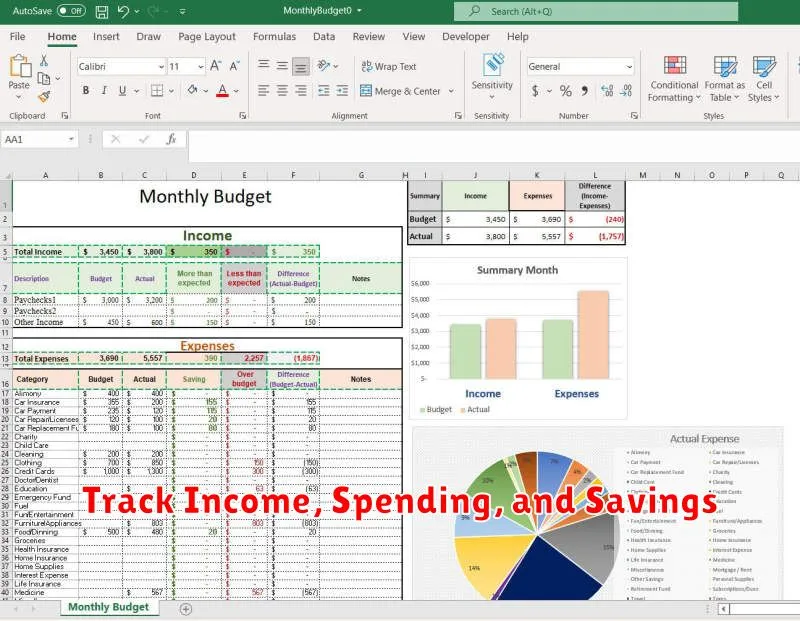

Track Income, Spending, and Savings

Tracking your financial progress monthly requires a diligent approach to monitoring your income, spending, and savings. This forms the bedrock of understanding your overall financial health and making informed decisions.

Begin by meticulously recording all sources of income. This includes your salary, any freelance work, investments, or other forms of revenue. Be sure to include both gross income (before taxes and deductions) and net income (after taxes and deductions) for a complete picture.

Next, carefully track your spending. This is where many find the process challenging. Consider using budgeting apps, spreadsheets, or a simple notebook to categorize your expenditures. Common categories include housing, transportation, food, utilities, entertainment, and debt payments. The more detailed your categorization, the better understanding you’ll have of your spending habits.

Simultaneously, monitor your savings. Note any contributions to savings accounts, retirement plans, or investment accounts. Tracking savings alongside income and spending will allow you to see the relationship between your earnings, expenses, and your ability to save and invest. Analyzing this relationship is crucial for creating a budget and achieving your financial goals.

Regularly reviewing your income, spending, and savings data will provide valuable insights into your financial behavior. This allows for identifying areas where you can potentially increase savings, reduce unnecessary expenditures, or explore opportunities to increase your income.

Use a Budget-to-Actual Comparison

Tracking your financial progress monthly requires more than just recording your income and expenses. A crucial step is performing a regular budget-to-actual comparison. This involves meticulously comparing your planned budget for the month against your actual spending and income.

This comparison highlights discrepancies between your financial plan and reality. For instance, you might have budgeted $500 for groceries but actually spent $650. This comparison immediately identifies a $150 overspend, allowing you to understand where your money went and adjust your future spending habits.

Employing a spreadsheet or a budgeting app can simplify this process. These tools often have built-in features for automatically comparing budgeted versus actual figures, providing clear visualizations of your spending patterns. Categorizing your expenses (e.g., housing, transportation, food) will make identifying areas of overspending even easier.

The key benefit of this comparison is its ability to inform your future budgeting. By analyzing the differences, you gain valuable insights into your spending habits and can make more accurate budget projections for the following months. Regularly analyzing this comparison ensures that your budget remains a dynamic and responsive tool, rather than a static document.

Don’t just focus on the negative aspects; also celebrate areas where you underspent. Identifying categories where you stayed within or below budget can provide motivation and highlight areas where you’re managing your finances effectively.

Set a Review Date Every Month

Establishing a consistent monthly review date is crucial for effective financial progress tracking. This allows for regular monitoring of your budget, savings goals, and overall financial health. Choose a date that works best with your schedule, perhaps the first or last day of the month, and stick to it diligently.

Scheduling this review is not just about looking at numbers; it’s about creating a habit of financial awareness. By setting aside dedicated time each month, you foster a proactive approach to your finances, rather than reacting to unexpected situations.

Consider using a calendar reminder or setting an alert on your phone to ensure you don’t miss your monthly review. This simple act of scheduling helps maintain accountability and reinforces the importance of regular financial self-assessment.

During your monthly review, you’ll assess your progress towards your financial goals, identify any areas needing adjustment, and celebrate your successes. This consistent monitoring allows for timely corrective actions, ensuring you stay on track to achieve your financial objectives.

The act of scheduling a monthly review, even if only for 15-30 minutes, is a powerful tool in building good financial habits and maintaining control over your finances. It’s a proactive step that ultimately contributes to long-term financial well-being.

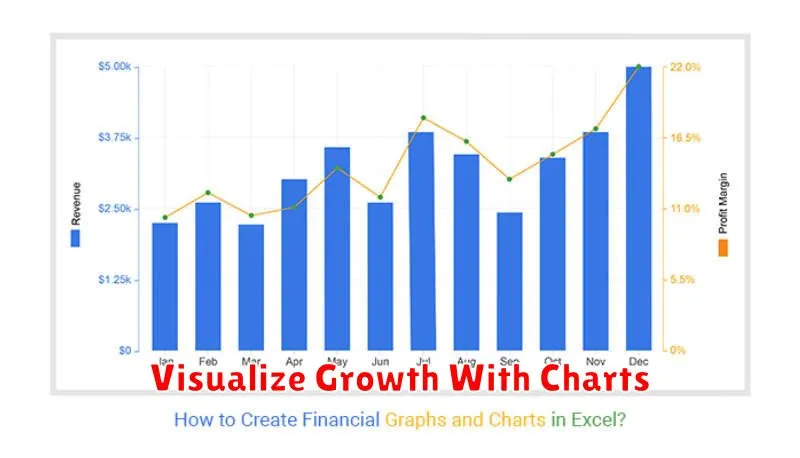

Visualize Growth With Charts

Tracking your financial progress monthly is crucial for achieving your financial goals. While spreadsheets provide detailed numerical data, visualizing this data through charts offers a powerful way to understand your progress at a glance. Charts can quickly highlight trends, successes, and areas needing attention.

Line charts are excellent for showcasing your net worth over time. By plotting your net worth each month, you can easily identify upward or downward trends and gauge the effectiveness of your financial strategies. The visual representation allows for quick comprehension of long-term growth.

Bar charts are ideal for comparing different categories of income or expenses month-to-month. This visual comparison allows you to easily spot overspending in certain areas or identify months with unusually high or low income. This facilitates informed budget adjustments.

Pie charts provide a clear picture of the proportions of your income and expenses. This visual representation helps you understand where your money is going and can identify areas where you can optimize spending or increase savings. It’s a great tool for visualizing your budget allocation.

Using a combination of these chart types offers a comprehensive overview of your financial health. The key is to choose the chart type that best represents the specific data you want to analyze. Remember, the goal is to create a clear and informative visual representation of your monthly financial progress, enabling better financial decision-making.

Adjust Based on Real Results

Monitoring your financial progress monthly isn’t just about collecting data; it’s about using that data to make informed decisions. After reviewing your budget and comparing it to your actual spending, you’ll likely find discrepancies.

These discrepancies offer valuable insights. Perhaps you consistently overspend in a particular category, like dining out or entertainment. Maybe you’re underspending in areas you had initially budgeted more for, such as savings or debt repayment.

Analyzing these differences allows you to refine your budget for the following month. If you consistently overspend on groceries, consider exploring ways to reduce costs, such as meal planning or utilizing coupons. If you’re consistently saving more than planned, you can explore adjusting your savings goals or allocating extra funds towards other financial priorities, such as investing or paying down high-interest debt.

Flexibility is key. Your budget shouldn’t be a rigid, unyielding document. Treat it as a living, breathing tool that adapts to your changing circumstances and spending habits. Regular adjustments based on real-world results are crucial for achieving your long-term financial objectives.

Remember, the goal is not to achieve perfect adherence to your budget every single month, but rather to use the data to continuously improve your financial planning and make progress towards your goals. Consistent monitoring and adjustment will significantly contribute to your overall financial success.

{kind=link}